How to Build a Personal Finance System That Actually Runs Itself

Disclaimer

Some links may earn us a small commission at no extra cost to you.

Click here to read our full affiliate disclosure.

Disclaimer

We believe in complete transparency with our audience.

Some links may earn us a small commission at no extra cost to you.

Please know that we only recommend products/services we have personally used, thoroughly researched, and genuinely believe can benefit our audience.

We are immensely grateful for every click and purchase you make through these links. Thank you for being a part of our community and for your continued support!

Click here to read our full affiliate disclosure.

Let's be honest. You've probably tried budgeting before. Maybe you downloaded an app, made a spreadsheet, or told yourself, “This month will be different". But then life happened, and the whole thing quietly fell apart by week three.

That's not a discipline problem. That's a system problem.

A personal finance system removes the part that causes problems, which is relying on motivation. When money management depends on how you feel, you'll always lose eventually. But when it runs on structure? It keeps working even when you're tired, stressed, or just don't feel like thinking about money.

This guide breaks down exactly how to build one from scratch.

Let's be honest. You've probably tried budgeting before. Maybe you downloaded an app, made a spreadsheet, or told yourself, “This month will be different". But then life happened, and the whole thing quietly fell apart by week three.

That's not a discipline problem. That's a system problem.

A personal finance system removes the part that causes problems, which is relying on motivation. When money management depends on how you feel, you'll always lose eventually. But when it runs on structure? It keeps working even when you're tired, stressed, or just don't feel like thinking about money.

This guide breaks down exactly how to build one from scratch.

Why "Just Budget Better" Is Terrible Advice

Most financial advice treats budgeting like a personality trait. Like some people are just "good with money" and others aren't.

That's nonsense.

The people who seem effortlessly good with money usually have one thing in common: they built a system and let it run. They don't have to constantly crunch numbers or rely on willpower. Their savings are automatically transferred. Bills are paid promptly, without a second thought. And their spending is kept in check with built-in guardrails.

Meanwhile, everyone else is reacting to the end of the month, to unexpected bills, to that uncomfortable feeling when you check your bank balance.

The fix isn't trying harder. It's building a money management system that does the thinking for you.

The 4-Step Personal Finance System (Simple Version)

Here's the framework we're going to build:

Awareness — Know where your money actually goes

Control — Give every dollar a job

Stability — Build a financial cushion

Growth — Put your money to work

Every step is designed to build on the previous one, so it’s crucial not to rush ahead, especially to step 4. Skipping steps can lead to financial instability, and we definitely want to avoid that trap!

Most financial advice treats budgeting like a personality trait. Like some people are just "good with money" and others aren't.

That's nonsense.

The people who seem effortlessly good with money usually have one thing in common: they built a system and let it run. They don't have to constantly crunch numbers or rely on willpower. Their savings are automatically transferred. Bills are paid promptly, without a second thought. And their spending is kept in check with built-in guardrails.

Meanwhile, everyone else is reacting to the end of the month, to unexpected bills, to that uncomfortable feeling when you check your bank balance.

The fix isn't trying harder. It's building a money management system that does the thinking for you.

The 4-Step Personal Finance System (Simple Version)

Here's the framework we're going to build:

Awareness — Know where your money actually goes

Control — Give every dollar a job

Stability — Build a financial cushion

Growth — Put your money to work

Every step is designed to build on the previous one, so it’s crucial not to rush ahead, especially to step 4. Skipping steps can lead to financial instability, and we definitely want to avoid that trap!

How to Build a Personal Finance System

Step 1: Awareness - Face Your Numbers

Most people avoid looking at their finances the same way they avoid the doctor. You know something might be off, and you'd rather not confirm it.

But here's the thing: awareness is the only step that costs you nothing. You're not changing anything yet. You're just getting a clear picture.

Do this today:

Pull up your bank statements from the last 30 days. Go through every transaction and sort them into rough categories: rent, groceries, transport, subscriptions, eating out, and random stuff.

That's it.

You might be surprised by what you discover. Maybe it's $150 a month in delivery fees you didn't clock. Perhaps you’re juggling four overlapping streaming services without even realising it. Maybe your grocery spending is double what you thought.

This is about gathering data. You can't steer a car with your eyes closed, and right now, you're driving blind.

Key numbers to track:

Total monthly income (after tax)

Fixed expenses (rent, loans, regular bills)

Variable expenses (food, transport, entertainment)

What's left over (or missing)

Once you know these, everything else becomes clearer.

Step 2: Control - Create a Budget That Doesn't Make You Miserable

The reason most budgets fail isn't lack of discipline. It's that they're built for a perfect, imaginary version of yourself, a version that never experiences a difficult week or needs to go on an unexpected dinner outing.

A good budget has flexibility built in.

The simplest structure that works for most people:

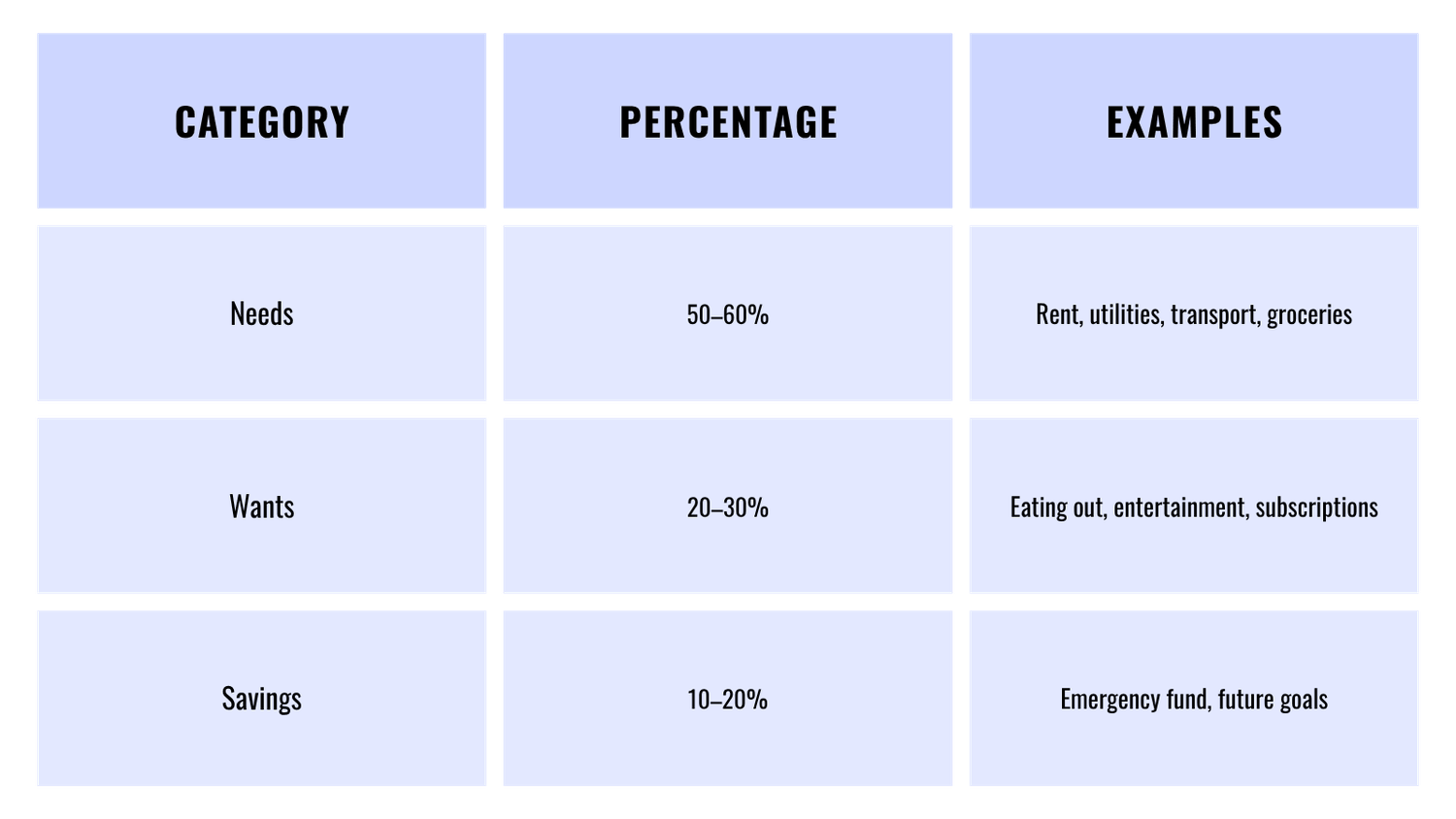

The 50/30/20 Framework (Adjusted for Real Life)

Step 1: Awareness - Face Your Numbers

Most people avoid looking at their finances the same way they avoid the doctor. You know something might be off, and you'd rather not confirm it.

But here's the thing: awareness is the only step that costs you nothing. You're not changing anything yet. You're just getting a clear picture.

Do this today:

Pull up your bank statements from the last 30 days. Go through every transaction and sort them into rough categories: rent, groceries, transport, subscriptions, eating out, and random stuff.

That's it.

You might be surprised by what you discover. Maybe it's $150 a month in delivery fees you didn't clock. Perhaps you’re juggling four overlapping streaming services without even realising it. Maybe your grocery spending is double what you thought.

This is about gathering data. You can't steer a car with your eyes closed, and right now, you're driving blind.

Key numbers to track:

Total monthly income (after tax)

Fixed expenses (rent, loans, regular bills)

Variable expenses (food, transport, entertainment)

What's left over (or missing)

Once you know these, everything else becomes clearer.

Step 2: Control - Create a Budget That Doesn't Make You Miserable

The reason most budgets fail isn't lack of discipline. It's that they're built for a perfect, imaginary version of yourself, a version that never experiences a difficult week or needs to go on an unexpected dinner outing.

A good budget has flexibility built in.

The simplest structure that works for most people:

The 50/30/20 Framework (Adjusted for Real Life)

The percentages aren't sacred. If you're in a high-cost-of-living city, your "needs" might creep to 65%. That's fine. The structure matters more than hitting exact numbers.

The one rule that actually matters: every dollar has a purpose.

When money remains in your account without a specific purpose, it tends to vanish. You might not even realise where it has gone. Designating each dollar to a category (even if that category is "fun money") eliminates the mystery.

A Practical Example

Say you bring home $4,000 a month:

$2,200 goes to needs (rent, food, transport)

$1,000 goes to wants (dining out, entertainment, clothes)

$800 goes to savings

That's not a restrictive budget. That's a plan. Big difference.

The percentages aren't sacred. If you're in a high-cost-of-living city, your "needs" might creep to 65%. That's fine. The structure matters more than hitting exact numbers.

The one rule that actually matters: every dollar has a purpose.

When money remains in your account without a specific purpose, it tends to vanish. You might not even realise where it has gone. Designating each dollar to a category (even if that category is "fun money") eliminates the mystery.

A Practical Example

Say you bring home $4,000 a month:

$2,200 goes to needs (rent, food, transport)

$1,000 goes to wants (dining out, entertainment, clothes)

$800 goes to savings

That's not a restrictive budget. That's a plan. Big difference.

Related Blog Post: How to Create a Simple Budget

Step 3: Stability - Build the Safety Net Nobody Talks About

This is the step most personal finance content rushes past to get to the exciting stuff (investing, wealth-building, etc.).

Without stability, one bad month can wipe out months of progress.

Priority One: Emergency Fund

Before you invest a single cent, you need liquid cash set aside for emergencies. Not invested. Not in crypto. Sitting in a separate savings account, boring and accessible.

First goal: 1 month of expenses

Long-term goal: 3–6 months of expenses

If your monthly expenses are $2,500, you're aiming for $7,500–$15,000 over time. Start with $2,500 as your first milestone.

This fund protects you from the domino effect, where one car repair or medical bill sends you into debt that takes months to climb back out of.

Priority Two: Handle Debt Strategically

If you're carrying high-interest debt (credit cards, personal loans), this is costing you money every single month. There are two popular ways to attack it:

Snowball method: Pay off the smallest balance first, regardless of interest rate. The psychological win of eliminating a debt keeps you motivated.

Avalanche method: Pay off the highest interest rate first. Mathematically optimal, you'll pay less total interest.

Either works. The best method is whichever one you'll actually stick with.

The most important rule: stop adding new debt while you're paying off old debt.

Priority Three: Separate Your Accounts

This small adjustment can lead to significant results.

Instead of having one account for everything, split your money into three:

Bills account — Fixed monthly expenses go here. Fund it once at the start of the month and don't touch it.

Spending account — Your day-to-day money for food, transport, and entertainment.

Savings account — Ideally at a different bank so it's not one click away.

When your spending account hits zero, you're done for the month. No accidental dipping into rent money. No end-of-month panic.

Step 3: Stability - Build the Safety Net Nobody Talks About

This is the step most personal finance content rushes past to get to the exciting stuff (investing, wealth-building, etc.).

Without stability, one bad month can wipe out months of progress.

Priority One: Emergency Fund

Before you invest a single cent, you need liquid cash set aside for emergencies. Not invested. Not in crypto. Sitting in a separate savings account, boring and accessible.

First goal: 1 month of expenses

Long-term goal: 3–6 months of expenses

If your monthly expenses are $2,500, you're aiming for $7,500–$15,000 over time. Start with $2,500 as your first milestone.

This fund protects you from the domino effect, where one car repair or medical bill sends you into debt that takes months to climb back out of.

Priority Two: Handle Debt Strategically

If you're carrying high-interest debt (credit cards, personal loans), this is costing you money every single month. There are two popular ways to attack it:

Snowball method: Pay off the smallest balance first, regardless of interest rate. The psychological win of eliminating a debt keeps you motivated.

Avalanche method: Pay off the highest interest rate first. Mathematically optimal, you'll pay less total interest.

Either works. The best method is whichever one you'll actually stick with.

The most important rule: stop adding new debt while you're paying off old debt.

Priority Three: Separate Your Accounts

This small adjustment can lead to significant results.

Instead of having one account for everything, split your money into three:

Bills account — Fixed monthly expenses go here. Fund it once at the start of the month and don't touch it.

Spending account — Your day-to-day money for food, transport, and entertainment.

Savings account — Ideally at a different bank so it's not one click away.

When your spending account hits zero, you're done for the month. No accidental dipping into rent money. No end-of-month panic.

Step 4: Growth - Now Let Your Money Work

Once you have awareness, a budget and a safety net, you can then focus on building wealth. Not before.

Pay Yourself First (Non-Negotiable)

As soon as money enters your account, you should transfer the amount you want to save to a separate account. Don’t wait for what remains at the end of the month because by then, there will likely be nothing left to work with.

Even 10% is powerful over a long enough timeline. $200/month at a modest return compounds into something significant over a decade.

Automate Everything You Can

Automation is the closest thing to having a financial superpower. Set up:

Automatic savings transfers on payday

Automatic bill payments so you never pay late fees

Investment contributions if you're at that stage

When the system runs automatically, you can't forget, procrastinate, or talk yourself out of it on a rough week.

Grow Your Income, But Don't Inflate Your Lifestyle

Saving and cutting expenses will only take you so far. At some point, increasing what comes in is the faster lever.

This doesn't mean you need a side hustle burning you out. It might mean:

Upskilling for a promotion or career move

Freelancing a skill you already have

Selling something you make or know

Step 4: Growth - Now Let Your Money Work

Once you have awareness, a budget and a safety net, you can then focus on building wealth. Not before.

Pay Yourself First (Non-Negotiable)

As soon as money enters your account, you should transfer the amount you want to save to a separate account. Don’t wait for what remains at the end of the month because by then, there will likely be nothing left to work with.

Even 10% is powerful over a long enough timeline. $200/month at a modest return compounds into something significant over a decade.

Automate Everything You Can

Automation is the closest thing to having a financial superpower. Set up:

Automatic savings transfers on payday

Automatic bill payments so you never pay late fees

Investment contributions if you're at that stage

When the system runs automatically, you can't forget, procrastinate, or talk yourself out of it on a rough week.

Grow Your Income, But Don't Inflate Your Lifestyle

Saving and cutting expenses will only take you so far. At some point, increasing what comes in is the faster lever.

This doesn't mean you need a side hustle burning you out. It might mean:

Upskilling for a promotion or career move

Freelancing a skill you already have

Selling something you make or know

Related Blog Post: 12 Ways to Make Real Income Online

But here's the trap people fall into: every raise gets immediately absorbed into a lifestyle upgrade. New car. Bigger apartment. Better phone. As your income increases, your expenses tend to rise in tandem, leaving things largely unchanged.

Keep your lifestyle increases smaller than your income increases. That gap is where wealth lives.

What Your Month Should Actually Look Like

Here's the full picture once your personal finance system is running:

Payday arrives — savings transfer fires automatically

Bills account is funded — fixed expenses are covered for the month

Spending account has your set amount — you know exactly what you have to work with

You live your life — no constant mental math, no guilt, no mystery

That's the whole system. It's not glamorous. It's not complicated. It's just a repeatable structure that makes the right thing happen by default.

Tools That Make It Easier (Without Overcomplicating Things)

You don't need fancy tools to make this work, a notes app and one savings account is enough to start. But if you want to add some structure:

Budgeting apps automatically categorise your spending

Digital banking tools let you create savings pockets or goals

Simple spreadsheets if you actually enjoy that kind of thing

The rule: use whatever keeps you consistent. The fanciest budgeting app in the world is useless if you open it twice and forget about it.

But here's the trap people fall into: every raise gets immediately absorbed into a lifestyle upgrade. New car. Bigger apartment. Better phone. As your income increases, your expenses tend to rise in tandem, leaving things largely unchanged.

Keep your lifestyle increases smaller than your income increases. That gap is where wealth lives.

What Your Month Should Actually Look Like

Here's the full picture once your personal finance system is running:

Payday arrives — savings transfer fires automatically

Bills account is funded — fixed expenses are covered for the month

Spending account has your set amount — you know exactly what you have to work with

You live your life — no constant mental math, no guilt, no mystery

That's the whole system. It's not glamorous. It's not complicated. It's just a repeatable structure that makes the right thing happen by default.

Tools That Make It Easier (Without Overcomplicating Things)

You don't need fancy tools to make this work, a notes app and one savings account is enough to start. But if you want to add some structure:

Budgeting apps automatically categorise your spending

Digital banking tools let you create savings pockets or goals

Simple spreadsheets if you actually enjoy that kind of thing

The rule: use whatever keeps you consistent. The fanciest budgeting app in the world is useless if you open it twice and forget about it.

Related Blog Post: The Best Personal Finance Tools for Beginners

Common Mistakes That'll Sink Your System

Even the best-laid plans can lead to common pitfalls.

Overcomplicating it. If your budget has 22 categories and requires 30 minutes to update weekly, you won't maintain it. Simpler is almost always better.

Skipping the stability phase. Jumping straight into investing when you have no emergency fund and high-interest debt is like running on a treadmill to get somewhere.

Ignoring small expenses. A $6 coffee every workday is over $130/month. Small leaks sink big ships.

Being too restrictive. A budget with zero breathing room isn't a budget; it's a punishment. Build in guilt-free spending money, so you're not constantly stressing about restraint.

Only doing it when motivated. Your system should work on your worst days, not just your best ones. That's the whole point of automation.

How Long Before You See Real Results?

Here's an honest timeline:

Week 1–2: You actually know where your money goes. That clarity alone reduces anxiety.

Month 1: You feel more in control. Decisions feel intentional, not reactive.

Month 2–3: You're saving consistently. The emergency fund is building.

Month 3–6: Real, visible progress. Your numbers are moving in the right direction.

It won't feel dramatic. But six months in, you'll look back and realise you went from financial chaos to a system that largely runs itself. That's the compounding effect of consistency, and it applies to habits just as much as money.

Your Personal Finance System Checklist

Before you close this tab, run through this:

✔ I know my monthly income and where my money goes

✔ I have a simple, flexible budget in place

✔ I'm saving a fixed amount every month

✔ I'm building (or already have) an emergency fund

✔ I have a plan for any debt I'm carrying

✔ My savings happen automatically

✔ I'm thinking about long-term growth

Even checking three or four of these puts you ahead of most people. The goal isn't perfection but forward momentum.

Final Thoughts

You don't need a new month, a new year, or a perfect financial situation to start. You need 30 minutes, your bank app, and a notepad.

Building a personal finance system is the single highest-leverage thing you can do with your money. Not finding the best investment. Not cutting every unnecessary expense. Building the structure that makes good decisions happen automatically.

Start with Step 1. Just look at your numbers. That's it.

Everything else follows from there.

Even the best-laid plans can lead to common pitfalls.

Overcomplicating it. If your budget has 22 categories and requires 30 minutes to update weekly, you won't maintain it. Simpler is almost always better.

Skipping the stability phase. Jumping straight into investing when you have no emergency fund and high-interest debt is like running on a treadmill to get somewhere.

Ignoring small expenses. A $6 coffee every workday is over $130/month. Small leaks sink big ships.

Being too restrictive. A budget with zero breathing room isn't a budget; it's a punishment. Build in guilt-free spending money, so you're not constantly stressing about restraint.

Only doing it when motivated. Your system should work on your worst days, not just your best ones. That's the whole point of automation.

How Long Before You See Real Results?

Here's an honest timeline:

Week 1–2: You actually know where your money goes. That clarity alone reduces anxiety.

Month 1: You feel more in control. Decisions feel intentional, not reactive.

Month 2–3: You're saving consistently. The emergency fund is building.

Month 3–6: Real, visible progress. Your numbers are moving in the right direction.

It won't feel dramatic. But six months in, you'll look back and realise you went from financial chaos to a system that largely runs itself. That's the compounding effect of consistency, and it applies to habits just as much as money.

Your Personal Finance System Checklist

Before you close this tab, run through this:

✔ I know my monthly income and where my money goes

✔ I have a simple, flexible budget in place

✔ I'm saving a fixed amount every month

✔ I'm building (or already have) an emergency fund

✔ I have a plan for any debt I'm carrying

✔ My savings happen automatically

✔ I'm thinking about long-term growth

Even checking three or four of these puts you ahead of most people. The goal isn't perfection but forward momentum.

Final Thoughts

You don't need a new month, a new year, or a perfect financial situation to start. You need 30 minutes, your bank app, and a notepad.

Building a personal finance system is the single highest-leverage thing you can do with your money. Not finding the best investment. Not cutting every unnecessary expense. Building the structure that makes good decisions happen automatically.

Start with Step 1. Just look at your numbers. That's it.

Everything else follows from there.

Ready to go deeper?

Trending

It's possible, even without an SSN.

Discover key qualities to consider when choosing right.

Learn what contributes to a successful business launch.

Deals & Promotions

You can also gain unlimited free access to Exclusive Content and Offers.

2026 © MitchelleO.D. All Rights Reserved.

Disclaimer: As an Amazon Associate, we earn from qualifying purchases. We may participate in additional affiliate networks or programs beyond Amazon.

Visit our Affiliate Disclosure Page to learn more.